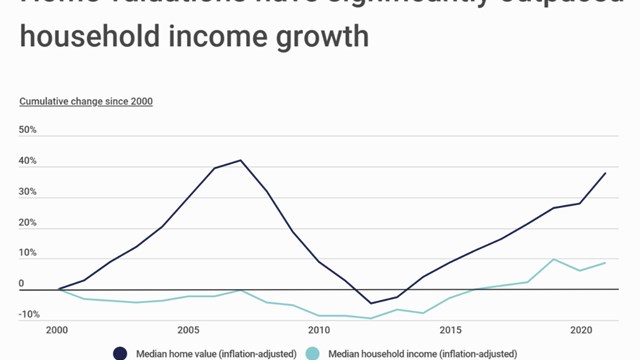

After nearly a decade of slow but steady progress back from the depths of the Great Recession, New Jersey is showing signs of real growth and prosperity. According to the U.S. Bureau of Labor Statistics, New Jersey added 61,000 jobs last year, which is the best year for private-sector growth since 2000. The gains continued into 2017, with 12,600 jobs added in January, bringing the unemployment rate to 4.6 percent, which is slightly below the national average, 4.7 percent. Governor Chris Christie, who inherited a 9.8 percent unemployment rate when he took office in 2010 recently commented, as quoted by NorthJersey.com: “I think we should stop the continuing drumbeat that somehow New Jersey has underperformed from a job perspective. New Jersey is outperforming the nation in 2016 in job growth and outperforming the nation in terms of unemployment rate as well.”

While the good news on the employment front in itself would be enough, it stands to reason that the effect of this economic improvement would extend to the real estate market – and it does. According to an article in the New York Times on March 17 of this year, New Jersey’s markets “are so brisk that many have less than three months’ inventory,” as reported by Jeffrey Otteau, president of the Otteau Group, an appraisal and advisory firm located in Matawan. “By way of comparison, in 2012, most markets had a four-to-eight month supply, a more typical range.”

The Structure of the Market

Approximately 66 percent of New Jersey residents own their own home, which can include a single-family home, a condo or co-op. The remaining approximately 34 percent are renters. Statewide, the overall vacancy rate for all dwellings is approximately 10 percent . Approximately 38 percent of dwellings were built between 1940 and 1969. Another 34 percent were built between 1970 and 1999, meaning nearly three-quarters of the residential housing stock in New Jersey is more than 17 years old. Of the total housing stock, approximately 45.5 percent are owned units in townhomes, small apartment buildings or apartment complexes of which 52 percent contain two bedrooms or less. Condo and co-op units are well represented in the state overall. Approximately 46 percent of housing units fall in the $208,000 to $416,000 price range.* (from www.NorthJersey.com)

According to information provided to The New Jersey Cooperator by New Jersey Realtors from their annual Townhouse-Condo Market Overview, pending sales are up 13.8 percent over same month in 2016, and closed sales are up four percent. Median sales price is up 1.8 percent, days on the market are down 14.7 percent, and supply has dropped 26.5 percent. The Times article goes on to say that “the dynamics driving demand vary from suburb to suburb, but industry experts cite several overall reasons for the busy winter. First, many buyers had been holding off on making a purchase until after the presidential election, largely because of uncertainty about the outcome. That pent-up demand was unleashed after November 8, and has been helped along by a mild winter.”

Bob Oppenheimer, president of New Jersey Realtors, says that “In total for 2016, there was an 8.8 percent increase in townhouse and condo closed sales over the entire 2015 year, increasing to 22,455 units over the previous 20,638 units. The median sales price was stable, with a negligible shift down 0.6 percent for 2016, prices sitting at $248,500 over 2015’s $250,000. For the beginning of 2017, continued low inventory could be the source of a slight decrease in new listings over February year to date numbers from last year. But numbers are comparable. Through January and February of this year, there were 5,911 new townhouse and condo listings throughout the state, whereas last January and February there were 6,042, a modest 2.2 percent decrease. This is likely an indication that the market is picking up steam in the first few months of the year with a significant 16.4 percent increase in year-to-date pending sales, up to 3,677 in February.”

The Otteau Market Report quoted in several articles also mentions that the supply of homes offered for sale remains constricted. This limits choices for home buyers. The number of homes currently offered for sale in New Jersey has declined by 5,400 units (-12 percent ) overall for all home types including single family, condominium, co-op and other units compared to one year ago. Today’s unsold inventory equates to a non-seasonally adjusted 5.4 months of inventory available for immediate sale, which is lower than the seven months of inventory available just one year ago. The decline in available inventory is a positive sign in the overall market.

Some Specific Examples

“In Jersey City,” says Oppenheimer, “February saw a 21.9 percent increase in days on the market until sale, with an average unit sitting on the market just fifty days which is an improvement over the 64 days similar units sat on the market at the same time last year. Townhouse and closed sales in Jersey City were also up 28.8 percent in February, up to 85 over last February’s 66. Mount Laurel is also seeing positive numbers in the first two months of the year, with median sales price for townhouses and condos at $161,000 in February 2017, a 15.4 percent increase over February 2016. Still, a slight dip in consumer confidence likely affected the condo market more than single-family homes since ownership tends to be more fluid, especially as younger buyers look toward this segment as a stepping stone to home ownership. Potential buyers are often continuing to rent until they are confident the economy is heading in the right direction.”

Another factor in speeding up home buying decisions and hence sales may be the rise in interest rates that began just after the election last year. The New York Times article from March 17 points out that many buyers decided to get going once rates began to rise which would account for the drop in available product in the New Jersey home market. The recent increase in the federal funds rate by the Federal Reserve, while not directly affecting long term mortgage rates in the short run, will lead to higher rates in the long run. The rate on a 30-year mortgage currently sits at around 4 percent. Just six months ago it was around 3.5 percent.

Otteau’s report also summarizes activity on the county level. According to data in the report, 81 percent of New Jersey’s 21 counties have less than an eight-month supply of available units for sale, which is considered to be the equilibrium point for home prices. Hudson County exhibits the strongest conditions in the state, with just 2.9 months of supply followed by Essex, Union, Morris, Middlesex, Bergen and Passaic counties, which all have fewer than five months of supply. Clearly, the northern part of the state is experiencing a more robust market than parts further south. Those counties with unsold inventory supply greater than equilibrium are located in the southern part of the state and include Cumberland, Cape May, Atlantic and Salem counties.

Adult Communities

New Jersey is among the most popular states in the nation for over-55 communities. Oppenheimer indicates that this segment of the market is also very healthy. “Adult communities finished strong in 2016 with median sales price, closed sales and pending sales up in year-to-date numbers. Throughout the state, year-to-date median sales price for adult communities was $175,000, a 2.95 increase over the 2015 price of $170,000. We continue to see adult communities sell extremely well throughout the state and the data assures us it is likely to continue throughout the remainder of 2017.”

Lastly, the Times article notes one unusual occurrence, a statewide spike in sales of homes priced between $1 million and $2.5 million, a market segment that has been sluggish in recent years. It could be a sign that high-income buyers are feeling extra confident with the talk of financial deregulation and tax reform. We can revisit that in 2018!

A.J. Sidransky is a novelist and staff writer for The New Jersey Cooperator.

{kind=link}

Leave a Comment